Equity-based compensation is a powerful engine for wealth creation, but only if it is navigated thoughtfully and diligently. Managed improperly, it can just as easily become an engine for frustration, unease, or despair.

As an executive’s career and compensation advance, there are more complexities to taxes, retirement planning, and wealth management goals to consider. Here are some of the most common questions executives have regarding the evolving terrain of their equity compensation packages:

What is equity-based compensation?

Any supplemental compensation to a base salary that comes in the form of company stock shares — or the right to buy them in the future (stock options) — is considered to be equity-based compensation. An employment contract with the company should contain details on how many shares of equity-based compensation is received each period, and the mix of stock vs. stock options to be received.

Equity-based compensation can be part of an annual salary or be granted as a contingent bonus if pre-set company performance targets are met during the period.

What are the advantages of equity compensation?

The biggest advantage of equity compensation is the opportunity to build long-term wealth via appreciation of the assets earned. Stocks have consistently risen above the rate of inflation for decades and owning stock in the company they work for aligns the company’s incentives and success with those of their executives.

Equity compensation is a pillar of the long-term wealth management plan of millions of accomplished executives. The key to converting this “potential wealth” into a stable wealth management plan is actively mitigating the key risks of concentrated stock positions. This is why the wisest executives partner with experienced financial and investment managers as their compensation structures gain in complexity and in stock-based pay.

What are the disadvantages of equity compensation?

Most forms of equity compensation have time restrictions on when the equity can be sold, and the proceeds received as cash. In addition, the value of the equity is highly variable and can also fall in price, even if the broad stock market is rising. There are no guarantees as to how much the equity compensation will hold or increase in value over time. As a result, this can create uncertainty or disappointment should the returns not meet initial expectations.

How are employees’ equity-based compensation taxed?

The most common taxation for equity-based compensation will be on par with an executive’s annual income, so the same rate as you pay on your base salary. Ordinary income tax rates will almost always apply to the raw amount of the award you were initially issued. If equity-based compensation is held for a long enough period, some or all of the gains the equity has achieved can be taxed as long-term capital gains — which usually represents a much lower tax rate than that of ordinary income.

How is stock-based compensation an expense?

From the perspective of the company that issues equity-based compensation to employees, the value of the equity granted is counted as a non-cash expense on the company’s income statement. While not an expense that reduces the company’s cash balances (as opposed to general wages), it is a real expense in that stock compensation dilutes the value of all existing shares of the company by a small amount.

To the executives who receive equity compensation, the stock awards are not classified as an expense but as income or investments (for the purposes of capital gains).

What if my company goes public before my vesting period is over?

This scenario can cause a couple of different outcomes. The company may offer to buy out your private company shares at their current market value prior to the initial public offering (IPO). More commonly, your private company shares will be automatically converted to the public shares once the company is listed on an exchange. This may or may not “reset” or increase the length of time the equity must be held before it can be sold for cash proceeds.

Is it appropriate to ask for more stock options instead of a raise?

A company’s philosophy around compensation structure is generally made at the top level and is applied to all employees equally for the sake of fairness. So, for example, if a company’s established policy is for executives above a certain tier to receive 30% of their base salary as stock options awards, then you won’t have the wiggle room to negotiate a higher percentage for yourself.

The more useful strategy would be to just ask for the raise in your base salary that you think you deserve; if you receive a bump in your base, you’ll also receive a bump in stock option awards.

Can incentive stock options be performance based?

While the structure of compensation packages will differ from company to company, generally there will be a separate category for performance-based compensation, regardless of whether that compensation comes in the form of stock options or cash. You could be offered a one-time bonus of restricted stock or stock options as a “retention bonus” if, for example, a company performance target is reached. This retention bonus would be contingent on you remaining with the company for a period of 1–3 years before that bonus award is fully vested.

What happens to stock options if I get fired?

In the event that you either quit or are fired for cause, you’ll generally forfeit all of your unvested stock options. If you are laid off, there is generally a window of time called a “post-termination exercise window” where you can exercise options and/or sell restricted stock units. That period could last for 3–12 months following your departure from the company. The details on such a window would be specified in your employment contract with the company or outlined as part of a broader severance package.

How can I draft a Cash and Equity Compensation Agreement?

It will be the company’s responsibility to draft equity compensation agreements and general cash compensation agreements, not you as an executive. The company will decide broadly how much of their compensation expense they want as cash and how much as equity-based compensation. Younger companies often lean more heavily on equity compensation, so as to save on cash expenses during the growing years of the company, and to strongly incentivize employees to strive for company growth.

Key information to be contained in an equity compensation agreement is the number of shares to be issued (or the percentage of base pay), the vesting schedule for restricted stock options, and any restrictions on how or when the equity compensation can be converted to cash (sold).

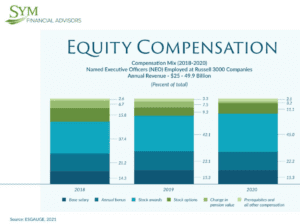

What do employers mean by salary ‘base, bonus, and equity’?

These are the three main components of executive compensation strategy as seen from the company’s eyes. The base salary will always be received as cash income. Bonuses are paid out either annually or quarterly, and are contingent on pre-specified company or executive performance targets being reached. Equity-based compensation is typically not contingent on performance, but is an annual award based on a percentage of the base salary.

In concert, these three pillars of executive compensation are how companies position themselves to attract and retain top talent.

Does EBITDA include stock-based compensation?

EBITDA is not a company income statement metric that is required to be reported under Generally Accepted Accounting Principles (GAAP) in the United States. Stock-based compensation is a non-cash expense to the company and recognized as such on the Income Statement.

Many public companies present a non-GAAP version of EBITDA to shareholders that excludes the (non-cash) expense of stock compensation, but this is a debated topic in the accounting community, as equity compensation is definitely a real expense as seen through the eyes of the company’s shareholders.

What is the meaning of RSU vesting over four years?

This is a common format for companies to construct their restricted stock unit (RSU) agreements with employees. Under a four-year vesting schedule, on the one-year anniversary of the RSU agreement being signed, the first 25% of the RSUs are considered vested and can be sold by the executive.

Following the one-year anniversary, the remaining shares will be vested according to either a monthly schedule (1/36th of the remaining shares vested each month for three years) or an annual schedule (25% of the total each year, with all vested after four years).

Many more highly detailed questions can arise for any executive dealing with the nuances of equity-based compensation on their own. It’s easy to miss small details without the help of a financial advisor who has seen hundreds of different pay packages and navigated the route to converting the potential wealth of equity pay into a cohesive investment and retirement plan. If you find yourself in that position, SYM can help. We have an entire team of executive compensation professionals that can answer your questions and make sure you’re on the right track toward success.

Disclosure: The opinions expressed herein are those of SYM Financial Corporation (“SYM”) and are subject to change without notice. This material is not financial advice or an offer to sell any product. SYM reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. This blog is for informational purposes only and does not constitute investment, legal or tax advice and should not be used as a substitute for the advice of a professional legal or tax advisor. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. SYM is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about SYM including our investment strategies, fees, and objectives can be found in our ADV Part 2, which is available upon request.