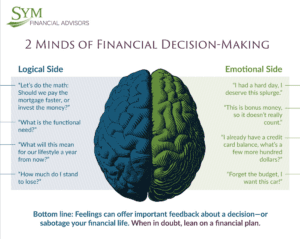

You might think that the hardest financial decisions are knowing which investments to pick, mitigating downside risk, or understanding how taxes might impact your returns. But there is one thing that can derail your investment portfolio even faster than poor investment choices and tax mistakes. That is the voice inside your head.

On the surface, our daily thoughts and emotions may seem trivial. However, they can trick us into chasing after investments that don’t make any sense. They can also sabotage our portfolios through poor decisions when the market gets volatile.

Below are five tips for better financial decision-making that can help you stay on course and avoid unnecessary losses.

Master Your Emotions

One of the worst things that can happen during a market downturn is letting fear get the best of you.

During the Great Recession from 2007 to 2009, the Dow Jones Industrial Average lost more than 50 percent of its value (1). People who had been saving for decades and who were close to retirement saw their nest eggs cut in half. Out of panic, many families rushed to cash out their retirement plans, thinking this action would prevent any further losses. In retrospect, this turned out to be one of the worst things you can do as an investor.

For those who cashed out their retirement savings prematurely, there were taxes and penalties. But the true cost of the decision was “locking in” those deep losses and putting many people in a position where they would not be able to recover. Compare that with those who held on tight through the Great Recession, and who saw their portfolios bounce back just three years later (and then go on to double in value again by 2019).

Since World War II, there have been 27 corrections in the stock market with an average decline of 14 percent (2). So far, the market has always recovered. More than that, it rose to new all-time highs (3). Investors who can ride out the short-term storms typically get rewarded on the other side.

Recognize Your Money Scripts

Your relationship with money may be more deeply rooted than you think. In their book Facilitating Financial Health, a father-son duo of Dr. Brad Klontz and Dr. Ted Klontz refers to these thought and emotion patterns as “money scripts,” or unconscious beliefs we hold about money.

According to the authors, there are four common types of money scripts (4):

- Money Avoidance – A deep-seated belief that money is bad and you’re not deserving of money.

- Money Status – Feeling like having money or not having money determines your place in society (and ultimately your self-worth).

- Money Worship – The belief that money will solve all your problems.

- Money Vigilance – Feeling anxious about money, protection, and safety.

Given that your money scripts have been with you since childhood, it’s unlikely that you will be able to ignore them. However, you can learn to recognize them and even use them to your advantage. For example, if your emergency savings are low, you could leverage the script of Money Vigilance to motivate you into saving more. The trick is to not deny your scripts. Instead, you can become aware of your personal money scripts, give them a productive role to play, and even turn them into strengths that can enhance your overall financial security.

Let the Facts Be Your Guide

Whether you’re chasing a rising investment like Bitcoin or dealing with a sudden market drop (like the single day 12.93% loss on March 16, 2020, during the start of the COVID-19 pandemic), it’s important to take a step back and look at the situation objectively (5).

The fundamentals that make up a solid investment are exactly the same during a recession as they are during the good times. For an individual investment, track key metrics such as earnings per share, book value, and debt to equity ratio. Understand what the company does, get to know its leadership through annual reports and quarterly performance calls, and keep an eye on its competition.

For investments in index funds, understand what the fund represents and what drives returns. Although past returns are never a guarantee for the future, they can provide some insight into how an investment has dealt with bumps in the market during previous market turbulence.

Finally, be cautious of news and opinions from major media gurus; they rely on scary headlines and controversial quotes for their paychecks. At the end of the day, they are not in the business of helping individuals reach their financial goals.

Stay True to a Long-Term Investment Strategy

Investing is a game that has turned many ordinary people into millionaires. That does not mean it’s a risk-free game. Every action and every investment comes with its own blend of risk and reward. Your job as an investor is to choose a portfolio that reflects both your goals and your risk appetite. The best way to accomplish that is to begin with a long-term focus.

History has demonstrated that a well-balanced and diversified portfolio of stocks and bonds has performed reasonably well over the past century. In one study, a well-diversified portfolio of 70% stocks, 25% bonds, and 5% short-term investments provided the best compromise between risk and reward from 2008 to 2014 when compared to an all-cash or all-stock portfolio (6).

Those who expect a reasonable rate of return and who have a comfortable mixture of investments for their risk tolerance typically are in the best position to ride out the markets.

The Cost of Emotions in Financial Decisions

Every investor, even those who have been in the market for a long time, can occasionally let their feelings get the best of them. One of the best things you can do for your finances is to work with a fiduciary financial advisor who believes in taking a comprehensive approach to financial life planning.

When your advisor is a fiduciary, you have hired a professional who will act in your best interest. In this role, the advisor won’t sell you products for the sake of making a commission. The strategies that they’ll recommend will come from an understanding of your specific financial goals and personal investment style (7). When you’ve got a fiduciary on your team, you can have conversations that go beyond which investments to pick.

Our team’s approach recognizes that financial markets go through periods of booms and busts. Our clients can expect the SYM team to ground them in their goals — and to examine well-rounded evidence to guide their investing decisions, today and into the future. If you are concerned about your preparedness for retirement or want a second opinion on your portfolio, schedule a call with a member of the SYM Financial team.

References:

- https://www.thebalance.com/stock-market-crash-of-2008-3305535

- https://www.forbes.com/advisor/investing/stock-market-correction/

- https://www.sym.com/are-you-experiencing-market-induced-vertigo/

- https://www.thinkingbigfinancial.com/what-is-money-script/

- https://www.thebalance.com/fundamentals-of-the-2020-market-crash-4799950

- https://www.sym.com/a-reminder-about-diversification-2/

- https://www.sym.com/advisor-as-fiduciary/

Disclosure: The opinions expressed herein are those of SYM Financial Corporation (“SYM”) and are subject to change without notice. This material is not financial advice or an offer to sell any product. SYM reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. SYM is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about SYM including our investment strategies, fees, and objectives can be found in our ADV Part 2, which is available upon request.